TL;DR — The 60-Second Version

- Indian banks can’t “just move to AWS” — RBI data localization, audit rights and concentration risk make a regulated private cloud for banks the default for core systems.

- Pure-private can’t absorb 10x festive-season spikes; pure-public fails on compliance and lock-in. The winner is a hybrid cloud strategy: sovereign private core + elastic public burst.

- For most banks the private-core race is VMware Cloud Foundation vs OpenStack vs Nutanix, with OpenShift as the cloud-native tier.

- No platform hits full AWS feature parity — serverless, managed-DB breadth and marketplace are the universal gaps, and those gaps are your burst candidates.

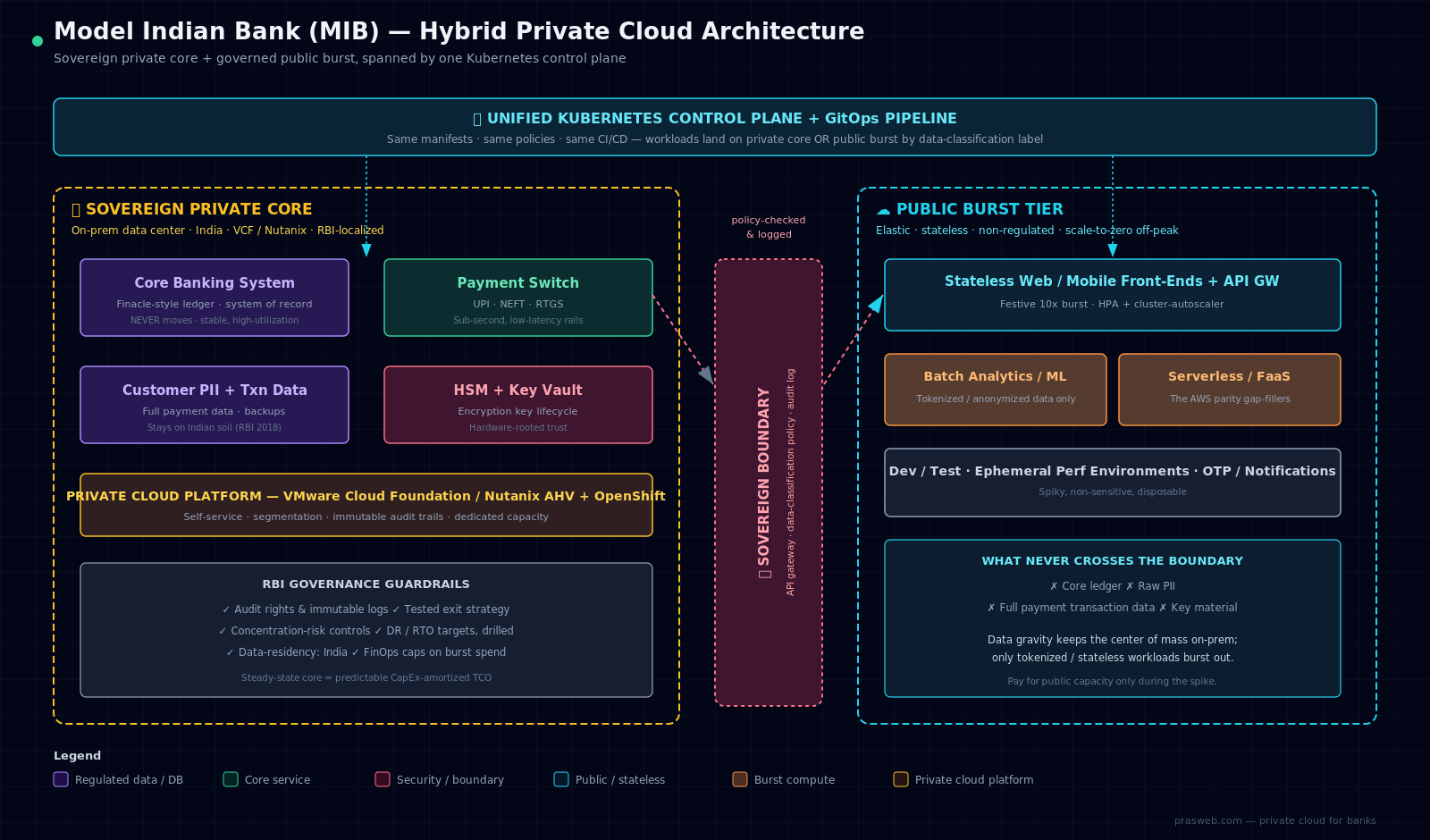

- Our fictional Model Indian Bank (MIB) lands on Nutanix for the private core, OpenShift for cloud-native services, and a thin public-burst tier behind a hard sovereign boundary.

It’s 11:58 PM on the eve of a major festival, and the head of infrastructure at Model Indian Bank (MIB) is watching a dashboard go red. UPI transactions are running at 9x the daily baseline. The mobile-banking tier is queuing logins. The VMware cluster that has faithfully run the bank for a decade is out of headroom, and there is no more headroom to buy tonight.

Everyone in the war room knows the easy answer everyone keeps shouting on LinkedIn: “Just go to AWS.” And everyone in that room also knows why that answer is wrong for a regulated Indian bank. This is the dilemma every BFSI architect lives inside — relentless pressure for agility and elastic scale, colliding head-on with a regulator who expects you to know exactly where every byte of customer data sits.

This post is the opinionated, regulation-aware playbook I’d hand any bank facing that exact wall. Building a private cloud for banks in India is as much a compliance decision as a technical one, so we’ll walk MIB’s decision journey, compare the real private-cloud platforms, score them honestly, and land on a defensible hybrid blueprint you can adapt.

The Regulated Bank’s Cloud Dilemma

The tension is structural, not technical. Your product teams want to ship features weekly and scale on demand. Your compliance team — backed by the RBI — wants deterministic control, full auditability, and a clean exit story. Both are right.

“Just go to public cloud” fails for Indian BFSI on three fronts — data localization, concentration and exit risk, and core-workload economics — each of which the next section unpacks.

The mistake isn’t choosing private or public — it’s treating it as a binary. Let’s start with why the private side is non-negotiable for a bank.

Why a Private Cloud for Banks Is Non-Negotiable in India

If you operate a bank in India, a robust private cloud isn’t a nostalgia project — it’s the load-bearing wall of your compliance posture. Here’s the reasoning your board and your regulator will actually respect.

⚖️ Regulatory nuance: This article is not legal advice. Indian banks can use public cloud, but regulated workloads require demonstrable controls around data residency, audit rights, exit strategy, outsourcing risk, and concentration risk. The recommendation here is architectural: keep the system of record and sensitive payment data in a sovereign private core unless you have a regulator-defensible reason not to.

1. RBI Data Localization (the 2018 mandate)

The RBI’s April 2018 directive (circular DPSS.CO.OD.No 2785/06.08.005/2017-18) requires full end-to-end payment transaction data to be stored in systems located only in India, with tightly controlled exceptions around permitted processing. That single requirement reshapes every architecture diagram. RBI data localization cloud requirements mean your system of record — and its backups — must sit on Indian soil, under your demonstrable control.

2. Data sovereignty and the outsourcing guidelines

RBI’s outsourcing and IT framework guidelines demand more than geography. The 2023 Master Directions on IT Outsourcing (RBI/2023-24/102, April 2023) and IT Governance (RBI/2023-24/107, November 2023, effective April 2024) — plus the new 2025 Outsourcing Directions for Commercial Banks — set the architecture bar banks must meet. You need contractual and technical guarantees around:

- Audit rights — the regulator and your auditors must be able to inspect the environment, including the provider.

- Exit clauses — a documented, tested ability to leave a vendor without stranding data or service.

- Concentration risk — no single provider failure should be able to take down critical banking services.

3. Latency for UPI, NEFT and RTGS

Payment rails are unforgiving. UPI’s user-experience and payment-switch latency expectations, plus NEFT/RTGS settlement windows, reward keeping the transaction core physically close to your switches and HSMs. A private cloud co-located with your payment infrastructure removes a whole class of latency and egress variability.

4. Cost predictability and operational control

Core banking is a steady, high-utilization workload — exactly the profile where owned capacity beats metered public cloud on TCO. Private cloud also gives you the controls auditors love: dedicated HSMs, hard network segmentation, immutable audit trails, and full control over the encryption key lifecycle.

⚠️ Caution: Don’t conflate “private cloud” with “the old VMware cluster we already have.” A regulator-grade private cloud means self-service, automation, segmentation, and audit hooks — not three admins clicking through vCenter. If you can’t provision a tenant via API with policy guardrails, you have virtualization, not a cloud.

📊 Market context: India’s hybrid cloud BFSI market was valued at USD 251.83 million in 2024, growing at 18.8% CAGR through 2031 (Cognitive Market Research). IDC estimates 80% of corporate banks in India migrated operations to cloud in 2024. The RBI has taken note: in November 2024, it announced plans to build a domestic cloud platform via IFTAS — its technology arm — specifically to give smaller banks and fintechs an RBI-governed, India-hosted cloud option. Additionally, the Digital Personal Data Protection (DPDP) Rules, notified in November 2025, add a further layer of data-handling obligations on top of RBI’s sector-specific requirements — affecting every cloud architecture decision for banks.

The Hybrid Case: Private Core + Public Burst

Here’s the uncomfortable truth that the festive-season war room teaches every bank: neither extreme works.

❌ Pure-private fails because you cannot economically size your data center for a 10x festive peak that happens a few days a year. You’d be paying for idle racks 360 days to survive 5. That’s capital lighting itself on fire.

❌ Pure-public fails because of regulatory friction, unpredictable egress costs, deep platform lock-in, and the concentration risk we already covered. Putting your core ledger on a hyperscaler is a compliance and exit-strategy nightmare.

✅ Hybrid wins — a sovereign private core for the regulated system of record, plus an elastic public-burst tier for stateless, non-sensitive, spiky workloads. This is the heart of any serious hybrid cloud strategy India conversation today.

What actually belongs in the burst tier?

- Stateless web/mobile front-ends and API gateways during peak campaigns.

- Notification, OTP-dispatch and read-only personalization services.

- Batch analytics, ML model training, and reporting on tokenized/anonymized data.

- Dev/test and ephemeral performance environments.

What never crosses the line: the core ledger, raw PII, full payment transaction data, and key material — data gravity meeting the sovereign boundary.

The glue that makes this practical is a consistent Kubernetes control plane spanning both sides, so the same manifests, policies and pipelines deploy whether a pod lands on your private core or a public-burst node pool. (See our related deep-dives on Kubernetes platform engineering and hybrid cloud architecture.)

Case Study: The MIB Decision Journey

MIB’s profile

- ~12 million customers, mid-sized private-sector bank.

- Explosive UPI and mobile-banking growth driving unpredictable peaks.

- An aging VMware data center nearing capacity and a hardware refresh cliff.

- A Finacle-style core banking system that must stay on-prem.

Drivers and constraints

MIB’s drivers were classic: cost of the looming refresh, festive-season elasticity, developer velocity, and a board that wanted a cloud story. The constraints were equally classic and far heavier:

- RBI localization — payment data must remain stored in India, with any external processing tightly controlled.

- Monolithic core — the Finacle-style ledger isn’t getting refactored for cloud-native any time soon; it needs a stable, performant home.

- Limited platform-engineering headcount — MIB has strong VMware ops skills but a small SRE/platform team. They cannot operate a hand-rolled distributed system at 2 AM.

MIB’s decision-criteria scorecard

MIB weighted its criteria honestly rather than chasing buzzwords:

- Migration risk from existing VMware estate — high weight

- Operational burden vs. current team skills — high weight

- RBI compliance & audit fit — high weight

- Cloud-native / container roadmap — medium weight

- 5-year TCO & licensing exposure — medium weight

- Public-cloud burst interoperability — medium weight

The journey: assess → PoC → boundary → pick

MIB ran a disciplined four-step path:

- Assess: classified every workload by data sensitivity and spike profile. Result — ~80% steady/regulated, ~20% spiky/stateless.

- PoC: stood up two private-cloud candidates side by side and a public-burst pattern behind a gateway.

- Sovereign boundary: defined exactly what data may cross to public, with policy enforced at the API tier and logged for audit.

- Pick: chose the platform combination with the lowest migration risk for the core and a credible cloud-native tier.

Outcome: a private core with minimal re-platforming, OpenShift for new cloud-native services, and a thin, governed public-burst tier for festive peaks — the full pick justified after the platform deep-dive.

Platform Deep-Dive: VCF vs Red Hat vs OpenStack vs Nutanix

This is where the VMware Cloud Foundation vs OpenStack and Nutanix vs VMware private cloud debates get real. Let’s map each to a bank like MIB.

VMware Cloud Foundation (VCF)

The incumbent’s natural upgrade path. VCF 9.0 (GA June 2025) bundles vSphere, vSAN, NSX and management into an integrated private cloud. For a VMware-heavy bank, it offers the lowest migration risk and the deepest ops familiarity. The trade-offs are significant post-Broadcom: documented 800–1,500% renewal price increases, a jump in minimum licensed cores from 16 to 72 per CPU (effective April 2025), and a shift to subscription-only bundles — a CloudBolt survey of 300 IT decision-makers found 95% said the acquisition disrupted their IT strategy. Banks with large VMware estates should model their 3-year TCO under the new pricing before committing to VCF as the long-term core.

Red Hat OpenStack Platform + OpenShift

OpenStack provides the IaaS layer; OpenShift delivers a best-in-class, supported Kubernetes platform. The current release — Red Hat OpenStack Services on OpenShift (RHOSO) 18.0, GA August 2024 — runs the entire OpenStack control plane on OpenShift, simplifying ops and unifying VM + container management under one platform. It now includes a VMware migration toolkit, making it an increasingly attractive destination for banks exiting VCF. This combo is excellent for banks committed to a container-first future and an open, portable stack, but demands more platform-engineering maturity than a turnkey HCI appliance.

Vanilla / community OpenStack

Maximum control, zero license cost, maximum operational burden. The community releases OpenStack twice a year — the current SLURP (long-term stable) release is 2025.1 “Epoxy” (April 2025), with 2025.2 “Flamingo” as the latest incremental. Globally, OpenStack powers 55+ million cores in production (2025 OpenStack User Survey). Tier-1 banks and telcos run it brilliantly — because they staff dedicated platform teams. For a bank with thin SRE headcount like MIB, self-supported OpenStack is a standing risk, not a saving.

Nutanix Cloud Platform (AHV)

Hyperconverged, appliance-simple, with the AHV hypervisor removing per-VM hypervisor licensing. Running AOS 7.5 / AHV 11.0 (December 2025), Nutanix shines on operational simplicity and a smooth migration story off VMware — making the Nutanix vs VMware private cloud question very live for cost-conscious, lean-team banks. Its public-cloud and container story is solid and improving. Encouragingly, Nutanix is already proving itself in Indian banking: Karnataka Bank deployed Nutanix NCP in December 2024 to power its critical applications and RBI-required CBDC platform.

Azure Local (formerly Azure Stack HCI)

If your bank is already Microsoft- and Azure-aligned, Azure Local (rebranded from Azure Stack HCI in November 2024) offers a consistent hybrid plane with Azure Arc governance. Important caveat for Indian BFSI: Azure Local requires mandatory monthly connectivity back to Azure for licensing telemetry. Even though workload data stays on-prem, RBI auditors have flagged mandatory external network dependencies on core banking infrastructure as a compliance concern — validate this explicitly with your RBI liaison and legal team before committing.

Here’s a minimal cloud-bursting node-pool definition — the kind of GitOps-managed config that lets MIB spill stateless front-ends to a public-burst pool while the control plane stays consistent:

apiVersion: cluster.x-k8s.io/v1beta1

kind: MachineDeployment

metadata:

name: mib-burst-frontend

labels:

tier: stateless-frontend

data-classification: non-pii # boundary policy: nothing regulated here

spec:

clusterName: mib-hybrid

replicas: 0 # idle by default — zero cost off-peak

template:

spec:

# Burst to public provider only when private core is saturated

failureDomain: public-burst-in-south

bootstrap:

configRef:

name: mib-frontend-bootstrap

infrastructureRef:

kind: PublicMachineTemplate

name: mib-burst-template

---

# HPA scales the deployment; cluster-autoscaler then grows the burst pool

apiVersion: autoscaling/v2

kind: HorizontalPodAutoscaler

metadata:

name: upi-frontend-hpa

spec:

scaleTargetRef:

apiVersion: apps/v1

kind: Deployment

name: upi-frontend

minReplicas: 6

maxReplicas: 60 # festive 10x headroom, off-prem

metrics:

- type: Resource

resource:

name: cpu

target:

type: Utilization

averageUtilization: 65

💡 Pro Tip: Set your burst node-pool replicas: 0 by default and let the cluster-autoscaler grow it only under real load. You pay for public capacity during the festive spike and nothing the rest of the year — that’s the whole economic argument for hybrid, expressed in 20 lines of YAML.

Author’s Verdict: Maturity & Overall Value Ratings

Let me be explicit about the rubric so you can argue with my scores:

- Maturity (1–10): stability, ecosystem depth, production track record in regulated enterprises, and quality of vendor support.

- Overall Value (1–10): capability-per-rupee, factoring TCO, licensing, operational burden, and fit for a typical mid-sized Indian bank.

These ratings are practitioner judgment scores for a mid-sized Indian bank like MIB, not benchmark results.

| Platform | Maturity (1–10) | Overall Value (1–10) | One-line take |

|---|---|---|---|

| VMware Cloud Foundation | 9 | 7 | Safest landing for VMware shops; you pay for that safety. |

| Red Hat OpenStack + OpenShift | 8 | 8 | Best open, cloud-native bet — if you have the platform team. |

| Vanilla OpenStack | 7 | 7 | Ultimate control and zero license; you own every 2 AM page. |

| Nutanix Cloud Platform (AHV) | 8 | 8 | Simplest ops + strong TCO; ideal for lean banking teams. |

| Azure Local (formerly Azure Stack HCI) | 7 | 7 | Great for Azure-aligned banks; vet sovereignty carefully. |

Commentary. VCF earns a 9 on maturity — nothing else has its regulated-enterprise track record — but a 7 on value because post-Broadcom pricing economics sting hard (800–1,500% increases, 72-core minimums). Red Hat and Nutanix both hit 8/8: Red Hat for an open, portable, container-native stack with its VMware migration toolkit, Nutanix for sheer operational simplicity and TCO. Vanilla OpenStack’s 7/7 is bimodal — a 9 for a tier-1 with a platform org, a 4 for a thin team. Azure Local’s 7/7 reflects real capability gated by sovereignty diligence — the mandatory Azure telemetry connectivity is an open compliance question in the Indian context.

The Metric That Matters: AWS Feature-Parity Scorecard

Maturity and value are necessary but not sufficient. The question your developers actually ask is: “What can I NOT do here that I could do on AWS?” That’s the AWS feature parity private cloud question, and it’s the most honest metric in the whole evaluation.

| Capability (AWS analog) | VCF | Red Hat | Vanilla OS | Nutanix |

|---|---|---|---|---|

| Compute (EC2) | 95% | 90% | 85% | 90% |

| Object Storage (S3) | 75% | 80% | 75% | 75% |

| Managed K8s (EKS) | 75% | 90% | 65% | 70% |

| Serverless / FaaS (Lambda) | 40% | 55% | 40% | 45% |

| Managed DB (RDS) | 55% | 60% | 45% | 55% |

| IAM | 80% | 85% | 70% | 75% |

| Autoscaling | 75% | 85% | 70% | 70% |

| Marketplace | 55% | 60% | 40% | 55% |

| Illustrative overall parity | ~70–75% | ~70–75% | ~60–65% | ~65–70% |

Notice the pattern. Compute parity is essentially solved. The universal gap is concentrated in three areas: serverless/FaaS, managed-database breadth, and marketplace depth. Most private platforms still lag AWS in Lambda-style scale-to-zero ergonomics and RDS-style managed database breadth.

Here’s the strategic insight: those exact gap workloads are your hybrid burst candidates. If serverless and exotic managed databases are weakest on-prem, run them in the governed public-burst tier — on tokenized, non-regulated data. The parity gap and the burst boundary line up almost perfectly.

⚠️ Caveat: Parity is not a requirement. These percentages are illustrative, not benchmarks. You don’t need 100% of AWS’s surface area — you need the ~20 services your workloads actually consume. Score against your usage, not the AWS feature catalog.

Recommendation: What MIB and Banks Like It Should Choose

Putting it together into an enterprise hybrid cloud architecture a bank can defend to its board and its regulator:

- Private core: VCF or Nutanix. For a VMware-heavy bank, these minimize migration risk and play to existing skills. Nutanix wins on TCO and simplicity for lean teams; VCF wins on incumbency and ecosystem.

- Cloud-native tier: OpenShift. Layer a supported, consistent Kubernetes platform for all new microservices, spanning private and public — pair it with a mature DevOps and GitOps practice.

- Vanilla OpenStack: only if you have the platform-engineering maturity. Brilliant with a real platform org; a liability without one.

- Public-burst tier: thin, stateless, governed. Front-ends, analytics on tokenized data, and serverless gap-fillers — never regulated data.

Governance must-haves (non-negotiable for BFSI)

- RBI-grade exit strategy — documented and tested, not theoretical.

- Audit hooks everywhere — immutable logs at the sovereign boundary, who-saw-what traceability.

- DR / RTO targets — defined, drilled, and evidenced.

- FinOps discipline — tag and cap the burst tier so festive elasticity never becomes a runaway bill.

MIB’s final pick

MIB chose a Nutanix-based private core (smooth VMware exit, lean ops, strong TCO) with OpenShift for its growing microservices estate, and a tightly governed public-burst tier for festive front-end scale and analytics. The Finacle-style core never moves; the sovereign boundary is enforced and logged at the API gateway. Next festival, the dashboard stays green — and the CFO isn’t paying for idle racks in March.

Key Takeaways

- Private cloud for banks is the compliance default — RBI localization, audit rights, and concentration risk make it so.

- Hybrid beats both extremes: sovereign private core for regulated workloads, elastic public burst for spiky stateless ones.

- Match the platform to your team: VCF/Nutanix for VMware shops, OpenShift for cloud-native, vanilla OpenStack only with real platform maturity.

- No platform hits full AWS parity — and the serverless/managed-DB/marketplace gaps are exactly what you should burst to public.

- Govern relentlessly: tested exit strategy, audit hooks, DR/RTO, and FinOps are the price of a defensible architecture.

Conclusion & Next Steps

There is no single “best” private cloud platform — there’s only the best fit for your regulatory posture, your team’s skills, and your workload mix. Anyone who tells you otherwise is selling something. The honest trade-off is between operational simplicity, openness, cost, and migration risk, and your weights are yours alone.

So do what MIB did: classify your workloads, define your sovereign boundary first, score the platforms against your real service usage rather than the AWS catalog, and build the hybrid blueprint that keeps your core compliant and your peaks elastic. Build your own scorecard — then defend it.

Planning your bank’s private or hybrid cloud journey? Subscribe to prasweb.com for deep-dives on cloud, microservices, and DevOps architecture — or drop your toughest sovereignty-vs-elasticity question in the comments.

Frequently Asked Questions

Why do Indian banks need a private cloud instead of just using public cloud?

A private cloud for banks is driven by regulation, not preference. RBI data localization mandates that payment system data be stored only in India, and the RBI’s outsourcing guidelines require audit rights, tested exit clauses, and control over concentration risk. A regulator-grade private cloud keeps the system of record, backups, and encryption keys under the bank’s demonstrable control while still enabling a hybrid public-burst tier for spiky, non-regulated workloads.

What does RBI data localization require for cloud architecture?

The RBI’s April 2018 directive on Storage of Payment System Data requires the full end-to-end transaction data of payment systems to be stored only in India. In practice this means your system of record and its backups must reside on Indian soil under your control, which makes a sovereign private core the default for regulated workloads and forces a hard, audited boundary around anything that bursts to public cloud.

VMware Cloud Foundation vs OpenStack — which is better for a bank?

It depends on team skills and roadmap. VMware Cloud Foundation offers the lowest migration risk and deepest operational familiarity for a VMware-heavy bank, at higher licensing cost. Red Hat OpenStack plus OpenShift is the stronger open, container-native, portable choice but demands more platform-engineering maturity. Lean teams should favour the turnkey path; banks with a real platform org can extract more value from OpenStack.

Is Nutanix a good alternative to VMware for a private cloud?

For cost-conscious, lean-team banks, yes. In the Nutanix vs VMware private cloud comparison, Nutanix Cloud Platform with the AHV hypervisor removes per-VM hypervisor licensing, simplifies operations through hyperconverged infrastructure, and offers a smooth migration story off VMware. Its public-cloud and container capabilities are solid and improving, making it a strong fit for banks prioritising TCO and operational simplicity.

Can a private cloud match AWS feature parity?

No private platform reaches full AWS feature parity, and that is fine. Compute parity is essentially solved, but serverless/FaaS, managed-database breadth, and marketplace depth remain the universal gaps. The strategic move is to treat those exact gap workloads as your hybrid public-burst candidates — running them on tokenized, non-regulated data — and to score platforms against the ~20 services you actually use rather than the full AWS catalog.